Some researchers and ex-students of the Department of Operations Research, Eötvös University Budapest participate in the R&D Project ”Research of quantitative models supporting procurement and sales portfolio management and development of an integrated analyzer, forecasting and optimizer tool system” (PIAC_13-1-2013-0012, Research and Technology Innovation Fund). The project is managed by IP Systems Ltd, which provides IT solutions in energy market. The modules developed in this project are integrated into the energy trading IT platform of this company.

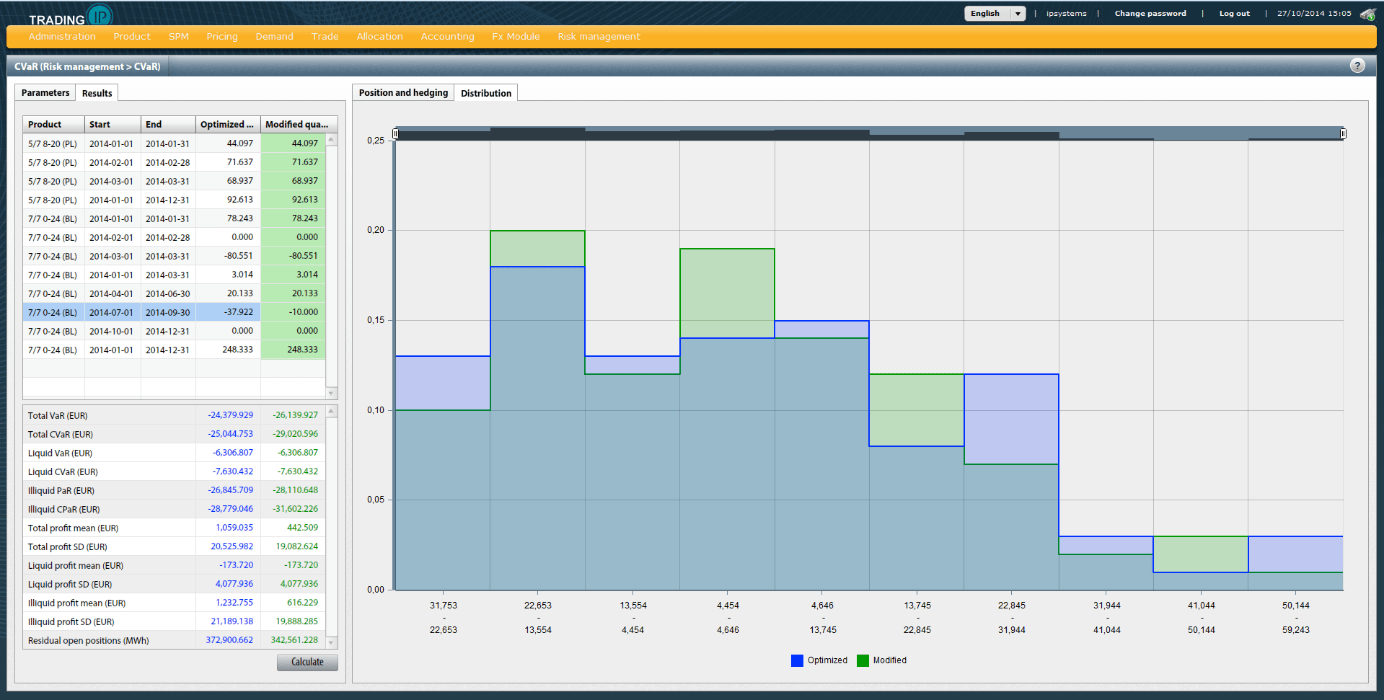

Two main parts of the project are related to operations research. The first module is the Price Risk Based Power Portfolio Optimization with Liquidity Constraints. The power portfolio consists of a procurement curve and several forward products. Our aim is to (re)hedge the portfolio in order to minimize its financial risk for a given time period (typically 10 working days).

The risk is measured by Conditional Value-at-Risk, which

- is a coherent risk measure (e.g., the sum of the risk of sub-portfolios cannot be less than the whole portfolio),

- gives more information on fat-tailed distributions,

- can be optimized easily.

The risk is presented by price curve scenarios. The finite liquidity of power markets are taken into account.

More details:

Click to access Madi-NagyGergely2014.pdf

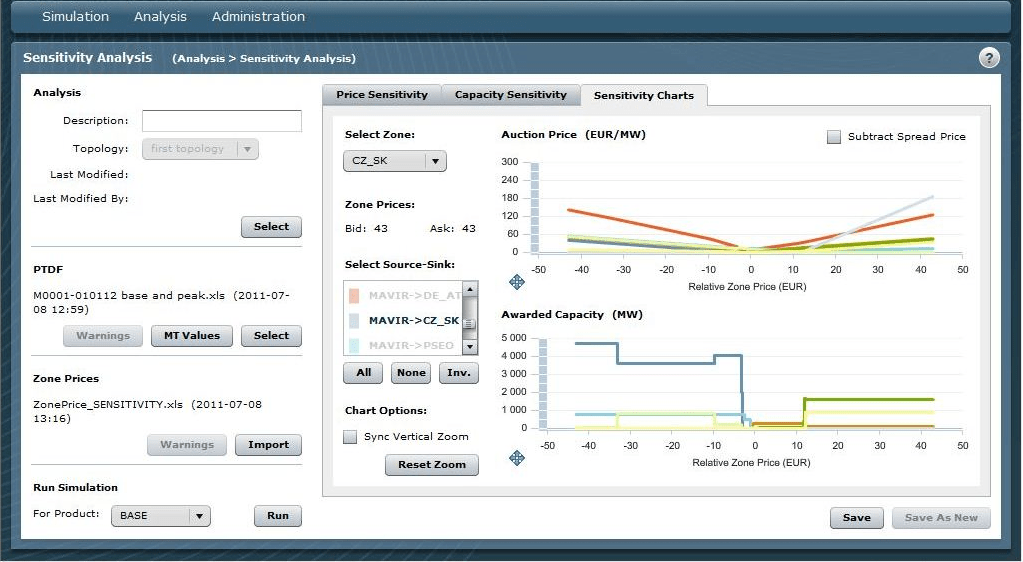

The other topic is Market Coupling Auction Simulation for Traders and Business Analysts. The present ATC model, the following FBMC model as well as their mixture are interpreted. There are several functions: the main physical properties of the network are presented, sensitivity analysis can be applied etc.