Digital assets have become an important part of modern finance. Initially introduced as a decentralized alternative to traditional currencies, they are now widely used and actively traded. Within the rapid growth of cryptocurrency markets, there has been a clear need for tools that help investors hedge risk or speculate on price movements, particularly futures and options.

Options on cryptocurrency futures offer new opportunities but also present major challenges. Their pricing is complicated due to high volatility and frequent price jumps. Classical models often fail to capture these dynamics and lead to large pricing errors. In light of these issues, we conduct a detailed comparison of pricing models to determine which approaches are the most effective.

We compare six option pricing models applied to European call options on Bitcoin and Ether futures contracts. The models include Black–Scholes, Merton Jump Diffusion, Kou, Heston, Bates, and Variance Gamma. Each of them is calibrated using market data from a regulated exchange on a highly volatile trading day — March 11, 2024. We consider a range of maturities, covering eight expiration dates: June, July, August, September, and December 2024, as well as March, June, and December 2025. All models are calibrated separately for each expiration date to capture maturity-specific market behavior.

To establish a starting point, we begin with the classical Black–Scholes (BS) model. This model assumes that asset prices follow a continuous stochastic process with constant volatility and no jumps. While elegant and computationally efficient, the Black-Scholes model struggles to accurately price cryptocurrency options. It assumes log-normal returns and constant volatility, which are rarely observed in crypto markets. Instead, prices often exhibit sharp jumps and heavy tails.

To better capture these features, we consider five more advanced models. The first is the Merton Jump Diffusion (MJD) model, which extends the Black-Scholes model by incorporating sudden price jumps through a Poisson process. Although it still assumes constant volatility, it provides a significant improvement in capturing discontinuities in price behavior. Building on this, the Kou model replaces the normal jump distribution with a double exponential distribution. This allows the model to account for asymmetric jumps. Another important extension is the Heston model, which introduces stochastic volatility through a mean-reverting process. Unlike previous models, it captures time-varying uncertainty in asset prices, a key feature in cryptocurrency markets.

The Bates model, also known as the stochastic volatility jump (SVJ) model, combines the strengths of the Heston and Merton Jump Diffusion models by including both stochastic volatility and price jumps. This hybrid approach offers high flexibility and is especially useful for modeling extreme events. Finally, the Variance Gamma (VG) model takes a different approach by modeling asset returns as a pure jump process. Without relying on Brownian motion, it captures the heavy tails and skewness

To evaluate the practical performance of each model, we compare their predicted option prices with actual market prices. In Figure 1, we present the results for BTC options with December 2025 expiration using two models: Black–Scholes and Kou. The differences between them are clearly visible. The BS model shows high pricing errors, particularly at the tails. The Kou model produces a much closer fit to market data across the entire strike range.

Figure 1: Pricing results using the Black–Scholes (left panel) and Kou model (right panel) for options on BTC futures contracts with expiry dates in December 2025.

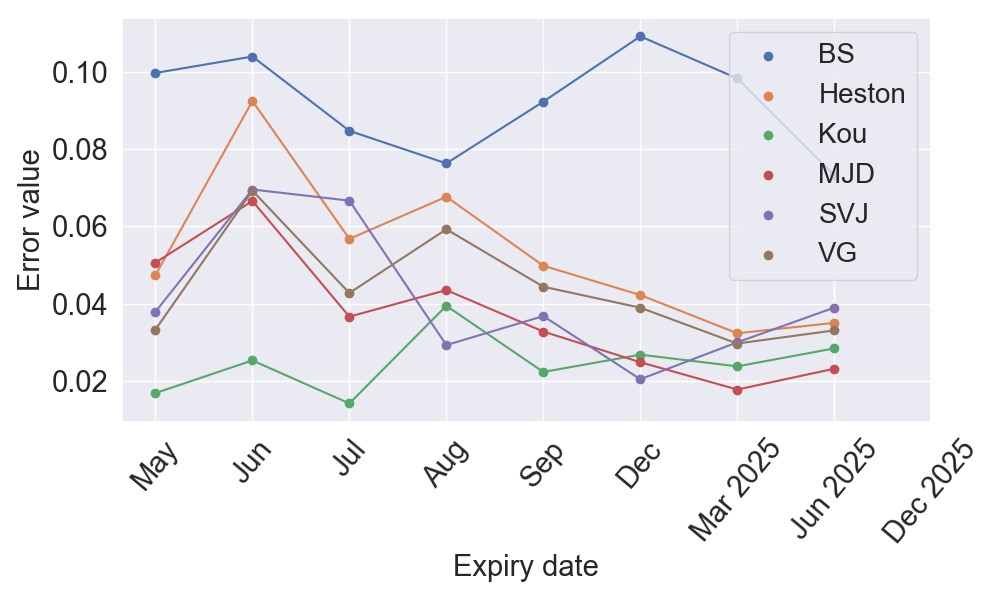

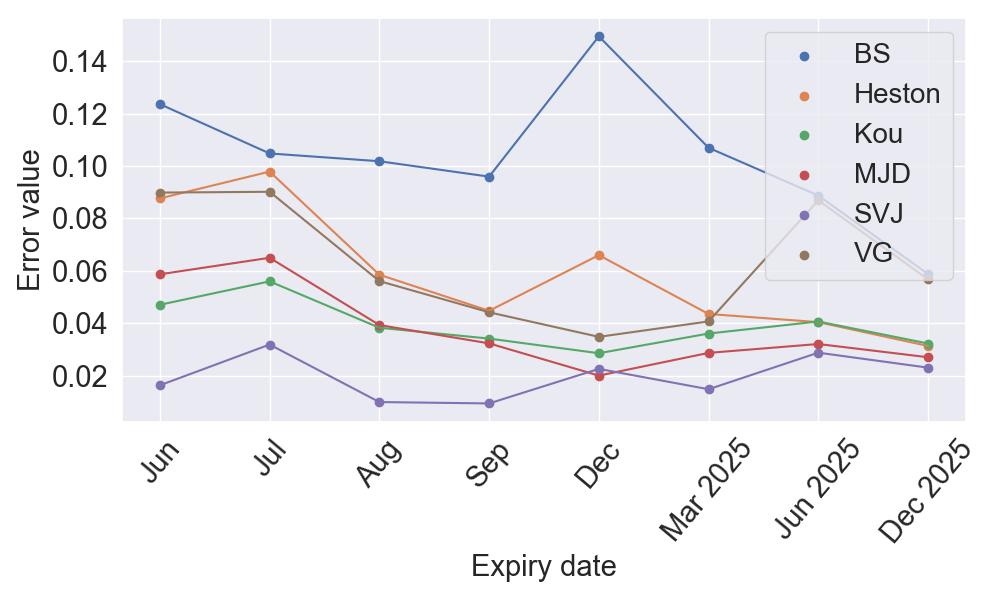

In addition to visual comparisons, we compute error values for each model. Figure 2 shows the mean absolute percentage error (MAPE) values across all maturities for BTC and ETH options. For BTC, the Kou model consistently achieves the lowest error, while for ETH, the Bates model performs best, highlighting the importance of including both jumps and stochastic volatility in pricing models for crypto assets.

Figure 2: Mean absolute percentage error values calculated for all the expiration dates for options on BTC (left panel) and ETH futures contracts (right panel).

The comparison of six option pricing models applied to Bitcoin and Ether futures reveals clear differences in their ability to reflect real market behavior. Black–Scholes, although simple and widely used, fails to capture the properties of crypto markets. The Merton Jump Diffusion model improves on this by including jumps, but it still performs poorly when volatility changes over time. Kou model, by allowing asymmetric jumps, provides a better fit for Bitcoin, which often experiences sharp price movements. Heston stochastic volatility model enhances pricing over constant-volatility models, especially for mid-range strikes and shorter maturities. The Bates model, by combining time-varying volatility and jumps, achieves the best performance for Ether across all expiries. The Variance Gamma model captures heavy tails and skewness effectively, and while it does not consistently outperform the others, it provides a useful alternative.

Overall, the obtained results clearly highlight that models incorporating both jumps and stochastic volatility better capture the unique characteristics of cryptocurrency markets, which are marked by extreme price fluctuations and irregular behavior. While no single model can be considered a universal choice across all maturities and error metrics, the Kou and SVJ models stand out as the best-performing models for both BTC and ETH options.

By Julia Kończal (Wrocław University of Science and Technology). The work supported by the NCN grant No. 2022/47/B/HS4/02139.